China is the world’s leading importer of soybeans, but changing dynamics and longer-term trends may pose questions for South American producer nations, which have seen years of reliable growth in the soy sector to meet rising Chinese demand.

After two decades of near-constant increases, China’s soybean imports have seen periodic dips and disruption since 2019, linked to the effects of the Covid-19 pandemic and African swine fever outbreaks in the Chinese pork industry, a major destination for soy as feed. Meanwhile, some analysts believe China’s soy imports may already have peaked.

These trends come alongside official plans in China to boost domestic soybean production and reduce reliance on imports, as part of a broader national food security drive – potentially an alarm bell for countries such as Brazil and Argentina, which find their main buyers in China.

In 2022, China’s total demand for soybeans was just over 115 million tonnes, over 80% of which was met with imports. Domestic soybean production reached 20 million tonnes last year, and the government has targeted an output of over 36 million tonnes by 2032 to reduce this reliance.

Several trade analysts have raised the possibility of potential impacts on South America from these changing dynamics, but key agribusiness figures in the region told Diálogo Chino that this situation is not a major cause for concern, at least in the short term.

“It does not seem likely that China will be able to significantly increase its own production, due to the water scarcity in its territory, and producers’ lower technical level and lack of adequate machinery,” said Rodolfo Rossi, head of the Argentine Soy Supply Chain Association (AcSoja). Along the same lines, the Brazilian National Association of Grain Exporters (ANEC) said that “the situation is not seen as a concern”.

However, interviewees raised other challenges in the global soybean market that will arise in the coming years. Among them are the consequences of increasing Brazilian production and the strong growth in the United States in crushing, the process of converting soybeans into other products.

Slowdown in demand

At the turn of the century, when it imported more than 10 million tonnes of soybeans, China accounted for 25% of global soybean purchases. Two decades later, these figures have multiplied several times over: in the past five years, China’s imports have ranged between 88 million and 100 million tonnes, accounting for around 60% of global trade.

“China has been the big market that has boosted world demand for soybeans,” said Gustavo Idigoras, head of the Argentine Edible Oil Association and Grain Export Centre (CIARA – CEC).

In the process, Brazil and Argentina, two of the main producers of soybeans, have benefited enormously, with China having become the main destination for their output, accounting for more than 90% of Argentina’s exports and 70% of Brazil’s shipments.

However, the situation has not always been smooth in recent years, and looking to the future, analysts see various reasons to anticipate a slowdown in the pace of China’s imports.

“China’s soybean imports will slow down and eventually decline through 2030 as a result of slower livestock production growth, continuous improvement in farming practices, and, more importantly, widespread adoption of a low-soymeal inclusion ratio in feed formulas nationwide,” said a recent Rabobank study. It believes this will have “profound impacts on the entire global supply chain”.

Another factor influencing this dynamic is the Chinese government’s drive to boost domestic soybean production, which reached 20 million tonnes in 2022. Its 14th Five-Year Plan (2021–2025) targets an output of 23 million tonnes by 2025, while the Chinese agriculture ministry forecasts that domestic production will reach 36.75 million tonnes in 2032.

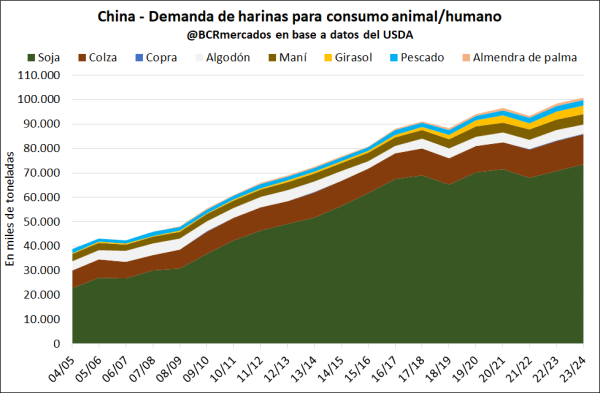

Given that soybeans will ultimately be processed, mainly for animal feed, it is also necessary to consider the outlook for soybean meal. “In recent years, there has been a diversification in China, where the growth in demand for rapeseed, peanut and sunflower meal has been faster than that of soybean meal,” explained Bruno Ferrari, an analyst at the Rosario Stock Exchange (BCR) in Argentina.

Ferrari said that while the growth in demand for soybean meal in China has slowed, unprocessed soybean demand has slowed even more, while other oilseeds are starting to grow a little faster or are maintaining their usual production levels. “That takes a little bit of space away from soybeans,” he added.

The BCR analyst’s explanation is reflected in official plans. In April, the Chinese agriculture ministry issued an action plan to reduce the use of soybean meal in animal feed, proposing that its share be reduced from the current 14.5% to less than 13% by 2025, Reuters reported.

Such a roadmap will “guide the feed industry to reduce the amount of soybean meal, promote the saving and consumption reduction of feed grains, and contribute to ensuring the stable and safe supply of grain and important agricultural products,” a ministry statement said.

No major impacts

Although the interviewees agreed that there is a slowdown in growth in soybean demand from China, none of them expressed concerns that the situation will generate abrupt changes in the export dynamics of Argentina and Brazil.

“I don’t think we should expect many implications for both countries as a result of changes in soybean demand from China,” said Gabriel Medina, a professor in agronomy at the universities of Brasilia and Goiás.

The academic’s view is shared by Sávio Pereira, director of the department of economic analysis and public policy at Brazil’s Ministry of Agriculture: “We are not worried,” he said, explaining that, among other factors, “the idea of changing the way animals are fed does not seem likely to happen in the short term.”

From Argentina, Gustavo Idigoras said that although there are analyses that indicate that China “may be reaching a plateau in its incremental demand for soybeans”, these should be taken “with caution”.

“Structurally, China is an importer of soybeans and will continue to be so,” Idigoras said.

Structurally, China is an importer of soybeans and will continue to be soGustavo Idigoras, head of the Argentine Edible Oil Association and Grain Export Centre

Echoing the responses heard by Diálogo Chino, BCR analyst Bruno Ferrari said that China’s domestic production targets “do not move the import market”, as it is a marginal increase in relation to the total volume. The gap between its production and demand is still “very large”, Medina added.

For Rodolfo Rossi, who represents the main actors in the soy supply chain in Argentina, “it will not be easy for China to achieve its forecasts due to the lack of improvements in local efficiencies.”

Third-country reports also support the outlook of the interviewees. In a recent article, the Australian Strategic Policy Institute noted that “competing land-use needs, including for other crops such as wheat and maize, make it difficult for China to escape from its dependence on soybean imports.”

The destination of surpluses

Against this backdrop, Brazil’s soybean production continues to grow. According to the latest US Department of Agriculture (USDA) estimates, the 2023/24 season is expected to see a 5% increase in total yield, up from 156 million tonnes in 2022/23 to 163 million tonnes. “And we still have a lot of new areas available for planting,” added Pereyra of the Brazilian agriculture ministry.

For Ferrari, the surplus generated by Brazilian producers will be destined for local industry: “The country has ways of continuing to generate virtuous production chains internally to introduce this merchandise and it is possibly the path they will follow in the future,” he said.

Something similar is happening in Argentina. Gustavo Idigoras explained that “there is a different strategy to that of Brazil, not focused on selling directly to China, but on selling processed products to other countries.” In fact, the country already exports large quantities of soy flours and oils to countries including India and Vietnam. Thus, according to him, potential increases in Argentine soybean production will go towards local industry, which has reportedly been working well below its potential.

Unlike Brazil, however, Argentina does not foresee strong increases in its local production, at least in the short term. Moreover, since its historic peak of the 2014/15 season – when output exceeded 60 million tonnes – the figures have tended to fall. The current agricultural cycle saw the worst soybean output recorded this century, at just over 20 million tonnes, driven by a harsh and prolonged drought.

In addition to this difference in soybean output, the two countries also diverge in terms of the destination of their production. Although both are heavily geared towards soy exports, Brazil ships most of its production as grain, while Argentina largely exports it with added value, in the form of processed flours and oils.

The fact that much of its production is destined for direct export does not mean that Brazil is not a central player in the processed products market. In fact, this year, all indications point towards it emerging as the world’s leading producer of soybean meal, displacing Argentina for the first time since the mid-1980s.

For Argentina, strong competition from Brazil is only one of the challenges in the short term. Rodolfo Rossi warns that the United States also foresees a “significant” increase in the processing of soybeans. “In any case, there are opportunities [for Argentine producers] in new markets in Africa and some Latin American countries,” he said.

With China’s push towards greater self-sufficiency in soybean production likely to take time and face various obstacles, Brazil and Argentina will have opportunities to remain significant players in the global market. Market diversification, boosting local processing and the exploration of new export destinations will be important areas for its agribusiness to explore.

But in a changing global landscape, and amid increasing climate volatility, the soy industry in both countries may need to show agility and invention if they are to maintain the stability – let alone growth – that has been so reliable in recent decades.

{kind=link}